The World Is Rewiring at Warp Speed

Oil distribution in a structural change, oil prices could drop. Accelerated Fed transmission. Inflation cooling. Market rally. New EU emerging. Ukrainian war enters a new phase.

The Market View

There is a pervasive feeling of uncertainty that unnerves the markets. Even the bears are cautious. As Stanley Druckenmiller said, there are times when bear markets are risky even for short sellers who try to gain from tactical trades by being caught in rapid upswings. Listening to CNBC commentators and their guests you get a sense that the mood is changing though. The average consensus, the “dot plot” of the views if you wish, is that we are now in the phase where earnings are downgraded - the last phase of the bear market.

The World Is Rewiring Its Transmission Pathways at Warp Speed

The speed with which the US economy is deteriorating alarmed many. Jamie Dimon spoke of the hurricane down the road. Elon Musk described the money loss at the plants in Texas and Germany as “gigantic money furnaces” and said he had a “super bad feeling”. A wave of layoffs and decisions to postpone hiring made the headlines in the past couple of weeks.

To me, the surprising factor is not the deterioration itself, but the speed. While early in the first half of the year market’s negativity has steadily progresses from bad to worse almost in a linear fashion, now it is in a gyration mode alternating from hope to depression inside the space of one week.

Many are making references to the past, like the 70s or 80s, predicting a long, dragging bear market, or at best a slow recovery. I beg to differ. The majority of the views miss one distinct element that makes our current times unlike the others. Not in principle, but in speed, the speed with which problems are solved (and created…).

We forget how far we have travelled in the past 50 years. The best example is the creation of the vaccine in less than a year from the start of the most dangerous pandemic in a hundred years. How did that happen? It’s not only because we have better science, but the collaboration speed has increased dramatically. Global communities of competence around the world pool their creative resources together much more effectively and faster. The entire world operates at high speed. The transformation applies not only to human connections, but the capacity of the planetary socio-economic system to adapt itself in the face of danger much more rapidly. This is more so evident in countries that have advanced technological infrastructure, although the other countries benefit over time from the collective ability to find solutions thanks to technology.

Going back to the subject of inflation, one of the beneficiary of accelerated transmission is the Fed. The communication of its strategy has triggered a series of events that reached deeply into the business and public psyche in record time. That change is visible in the borrowing rates and the adjustment of business hiring stance. This will have an impact on inflation because the purchasing patterns will gear toward being thriftiness. This in turn softens the case for big interest rate hikes.

Will Oil Markets Reprice to Reflect the New Distribution Structure?

However, the biggest and the most important change of all is the redistribution of oil supply. The sanctions on Russian oil caused a surge in oil prices because the supply on the European markets and elsewhere has dropped. Tankers carrying Russian oil have been refused entry in major ports. The higher oil price has boosted the inflation, naturally.

As the mid term elections in the US are close, president Biden has launched a campaign against the big oil companies urging them to produce more oil and asked the congress to suspend the gas tax for three months, which amounts to about 18cents per gallon.

This measure has been heavily criticised because it is believed it will stimulate consumption adding to the inflationary pressures. Nevertheless in the week of 13th of June the oil price dropped by ~14%. Why? I believe this has nothing to do with the gas tax; it is because the market has become aware of the scale of Russian import of oil by India.

India has increased imports of Russian oil by more than 25-fold since the start of the war, buying an average of 1 million barrels a day in June, compared with 30,000 in February, according to Kpler data. That is equal to more than a quarter of Europe’s imports of Russian crude and crude products, according to International Energy Agency data. (WSJ)

But what is more interesting is the import price: $37, even $34. If India and China import massive amount of oil directly from Russia, then why is the oil so expensive in the US and Europe? Both Russia and Opec produce oil at record levels. The oil that is not purchased by India and China through normal channels has to find a home somewhere else.

This is why I believe the drop of oil energy stocks is not temporary, the oil price will slide and consequently the inflation will come down faster than feared. In contrast, natural gas is a different ball game for Europe, and still a problem considering the lack of LNG infrastructure.

The labour market is also changing rapidly. It’s like a nervous system reacting to new stimuli. Reports describe the situation with alarming narrative ‘It’s almost unbelievable’: People are having their job offers rescinded days before they start”. This development is helping the Fed’s stated goal of cooling the employment market toward a balance between job seekers and job openings.

High unemployment doesn’t automatically translate into high inflation. As an example, the labour market in Australia is tight, but prices are relatively stable compared with the rest of the world. RBA has raised the interest by 0.50% as expected, however the tone of its statement is not that hawkish:

Inflation is forecast to peak later this year and then decline back towards the 2–3 per cent range next year. As global supply-side problems continue to ease and commodity prices stabilise, even if at a high level, inflation is expected to moderate.

Statement by Philip Lowe, Governor: Monetary Policy Decision, RBA, 5 July 2022

World Financial Systems Are Interconnected Like Never Before

To put things into perspective and demonstrate how vastly different are the worlds of 2020s and 1920s, let’s consider the state of working relationship between the major financial systems. In 1929, Australia elected James Scullin as Labour prime minister who inherited a large deficit due to lower revenue from wool and wheat. The treasurer was thought to have a difficult task in securing a loan because “Both the London and New York markets are now closed to Australian government borrowing, and it is doubtful whether money can be raised in Australia at an interest rate less than 6%” (Barron’s Averages, 12 December, 1929). The world of 1920s is one of closed markets, lacking sharing of information and cooperation, except for high level meetings made for posturing rather than for solution finding. The rigidity and opaqueness of the financial systems on the global stage were main contributors to the making of the Great Depression. That is not the case today. One the other hand we have bitcoin now and crypto. Risks are never in short supply.

The technology infrastructure based on cloud computing wrapped around the globe also contribute to the fast adaptation of the supply chain. Ryan Petersen, the CEO of Flexport tweeted recently: “Ocean freight prices are down almost 50% from the last year’s peak and still falling fast. Ocean carriers have ships orders that will add more than 30% more capacity to the global carrier fleet in 3 yrs.”

In conclusion, inflation may come down faster than expected.

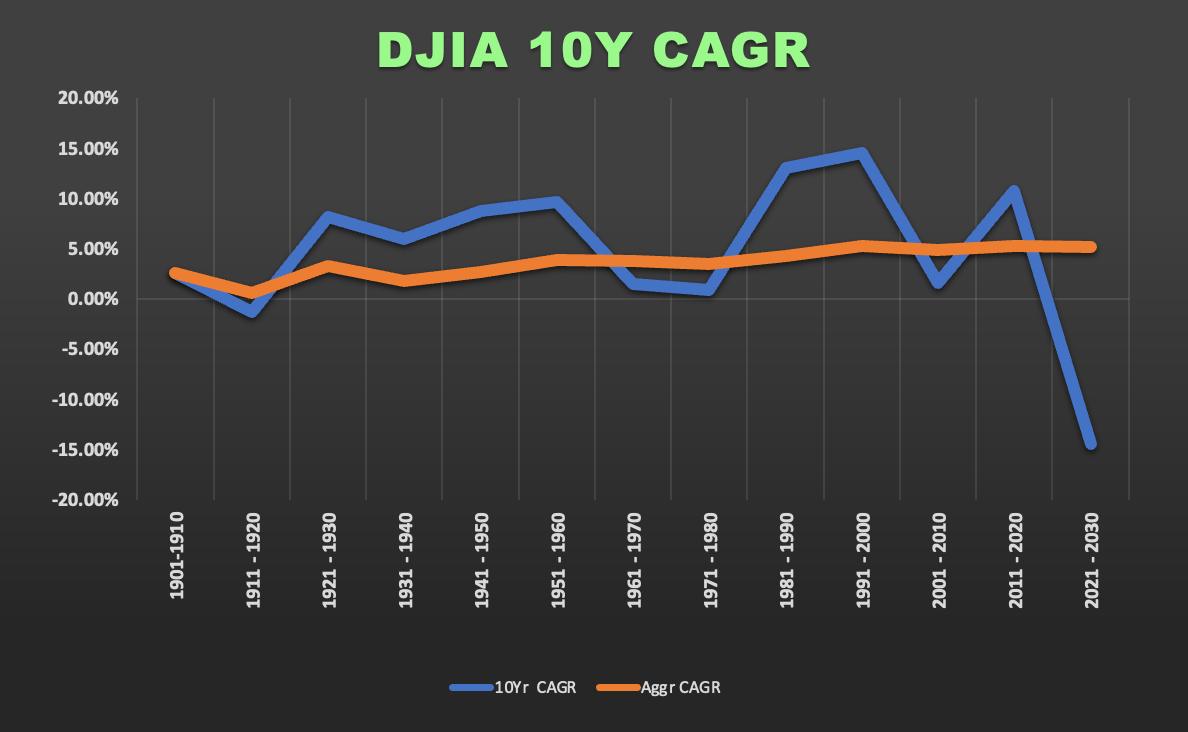

Expecting a Rally

The rapid fall of DJIA is so deep that a rally is needed to bring the indicator back to the 100 years average growth rate. The market is expensive, but the speed of deterioration is too high to remain at this level. If we look at the average DJIA 10yr CAGR, the current compound growth rate for this decade is far below the average, meaning the market is likely to readjust upwards.

I am not suggesting that we will hit new highs, but as a minimum, not go to much lower levels. The long term “natural” level is 27,655, still way below 31,097 as of close of business last Friday. The chart points to a volatile period in which the markets will find a new equilibrium around the long term average. The monthly VIX chart below shows an unusual compactness of the upward trend, which indicates volatility could last for a while.

However, I believe that we are in for a bump in the growth rate due to a new generation of technological wave that comes once every 20 years. We are just about to start a new wave, the most powerful to date. I will discuss that in a future post.

Also, on a positive note, an encouraging statistical observation: when the S&P 500 has fallen at least 15% the first six months of the year, as it did in 1932, 1939, 1940, 1962 and 1970, it has risen an average of 24% in the second half, according to Dow Jones Market Data (WSJ 1 July, 2022).

Geopolitical Watch

Last week’s G7 meeting in Germany, coupled with the admission of Sweden and Finland in NATO, is a display of collaboration united against Russia. Despite all the contradictions, the delays, the indecisions, this international alliance that spans across the world if you include South Korea, Japan, Australia and New Zealand, is an energetic, creative and productive group that will outlast, outdo and overcome Russia.

When Putin started the war he thought of one enemy, Ukraine, and a vague, feeble alliance that is incapable of intervening in the “special military operation”. This will go down in history as one of the biggest geostrategic miscalculation in modern times. The capacity of the Western alliance to produce armament is vastly superior to Russia’s and much more modern. The cooperation of European countries, each contributing with resources in form of money or military equipment is increasingly having an impact on the Ukrainian theatre.

The Ukrainian war is entering a new phase. Russia has gained Luhansk region, but meanwhile Ukraine has a new batch of modern artillery and trained military ready to use long range HIMARS. Soon Ukraine will have modern anti-missile systems that will limit the ability of Russia to bomb Ukraine at will with long range missiles. Kherson is key, this is the place to watch.

Notably, France and Germany have changed their tune and switched from a measured stance to a more open and active support for Ukraine. France has even published the [edited!] exchange between Macron and Putin to demonstrate that France is really on the side of Ukraine. Post G-7 clear willingness of France and Germany to assist Ukraine, signals the formation of a new Europe. The Founders had to acknowledge the influence of the Eastern and Northern Europe and the fact that they lost the oversized influence they had in the past. They also see the huge potential of rebuilding Ukraine project and the fact that EU + Ukraine will become a much more powerful world actor. Post-Ukraine war, expect a new world order of a different kind.

Putin’s mistake will cost Russia dearly with a long term isolation from the creative economies of the world as he destroyed in one single swoop the trust of his government which will have a long shadow over the world’s perception of Russia’s national character. It will take time to get back.

Arguably, the Ukraine war is having an indirect impact on the stability of Central Asia. The recent developments in Uzbekistan may have been possible (or encouraged) as the result of Russia’s concentration of its resources in Ukraine. Some analysts believe that Turkmenistan is in an even more volatile situation ready to burst.

Another development on the sideline is the active presence of Turkey in Syria. As I highlighted last week, the re-alignment of Saudi Arabia and Turkey may be aimed at countering the influence of Iran, in addition to improving the economic relationship. This is something to watch closely.