Tesla 2023 Q1: The Big Miss

Tesla 2023 Q1: The Big Miss

Overlooking the emerging EV enterprise business market.

Tesla is the most talked about listed company. That’s not surprising. What is surprising is what is not talked about Tesla. FY23 Q1 earnings call was interesting and dry at the same time. The questions were dull, but the answers were interesting. It is curious how this company with one of the most innovative and impactful strategy in the world is mostly debated about whether to buy it, sell it, or hold it, based on share price, momentum, production and deliveries.

I am not going to go into financial details, but I will highlight the overlooked and undiscussed big strategic elements that Tesla is executing, flawlessly so far, that make me believe Tesla is becoming a new type of planetary corporation suited for the new AI era. The overall strategy, if successful, will likely make Tesla the most valuable company by 2030.

I use the term “planetary” as opposed to “transnational” to describe a private economic entity that functions in real-time as one coherent, horizontally layered network spread across the planet, on the ground and in the sky, very different from hierarchical, organisationally vertical, compartmentalised, with multiple sand-boxes ground-based structures typical of the large global corporations typical of the post-industrial era.

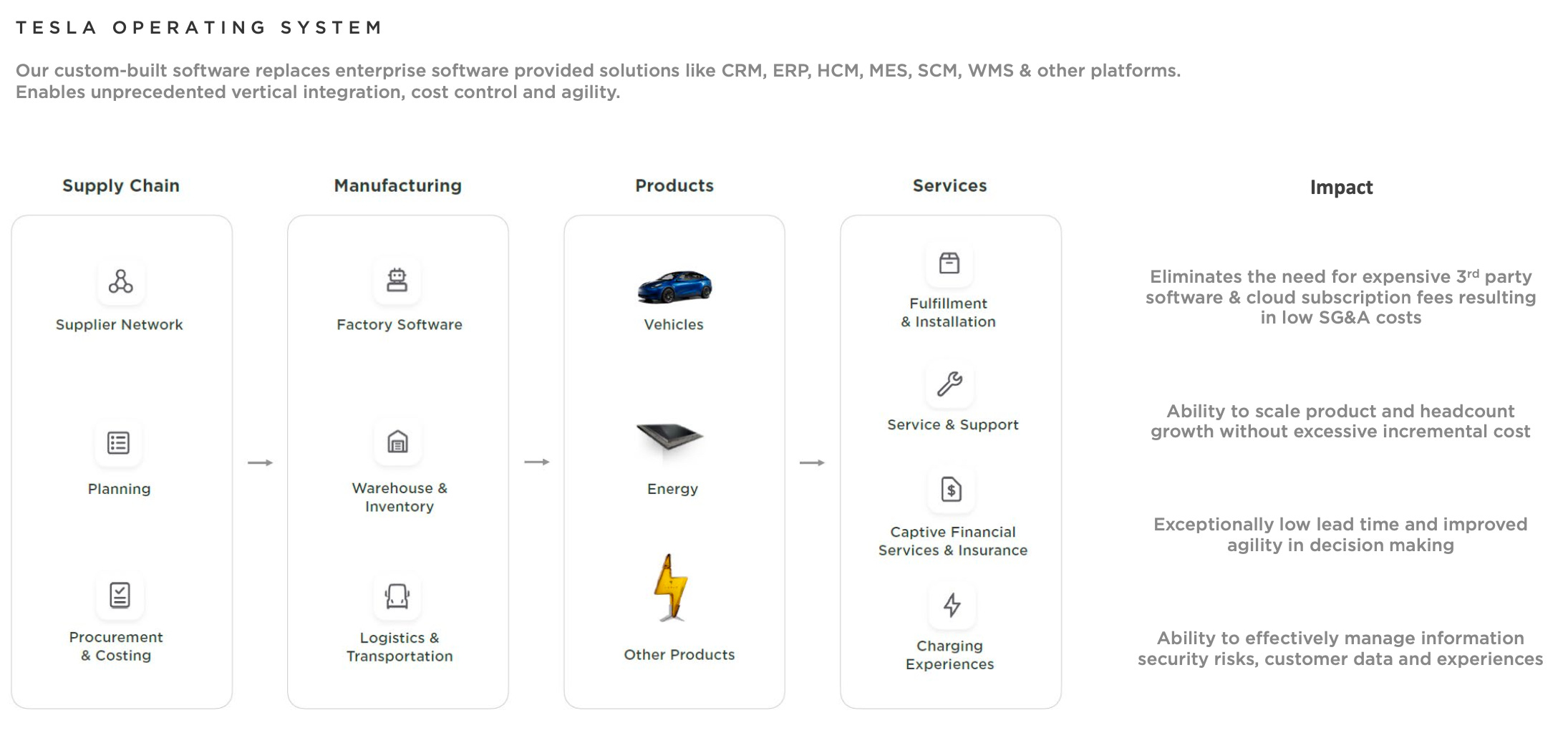

Tesla’s Salient Strategic Elements

First of all, Tesla has a cloud based business operating system architected like an enterprise software system with interconnected, but distinct functions. That structure was part of the 2023 Q1 results presentation, mostly ignored by the analysts:

Secondly, Tesla is built like an energy company that powers everything inside the company for its own cars, and outside the company for its customers. No other company comes close to this level of broad synergy.

Thirdly, Tesla is built like a vast information network powered by high performance computer chips that continuously gathers real world data for on-going improvements that are made in rapid succession (FSD relentless upgrades are proof of Tesla’s responsiveness to real-world data driven feedback).

Fourthly, and this is so often overlooked, Tesla is part of a larger planetary system which includes Starlink, Twitter (actually X.com, which includes Twitter and X.AI) and SpaceX. But this is a story for another time.

When discussing the company financials if you stop at counting the products made and delivered, analyse its pricing and current operating and net income margins ignoring the agility and built-in both synthetic AI and human AI, you are missing the real value of the company.

Treating Tesla like a car company is a misplaced simplification (“it bends steel, then it must be a car company” as Jim Lebenthal once said on the CNBC Half-Time Report show).

Many analysts see the pricing tactical decisions as weakness, instead of strength. The power of its business operating system is reflected in having the highest margins in the industry and the ability to make adjustments depending on the state of the demand locally and across the globe, and of course, competition. Tesla’s executives provided ample details in their answers, but it seems many of these details just got lost and never made into the media reports. I will briefly list them below, with the most important part at the end.

Costs Control Is Not an Accounting Imperative

Cost control is part of Tesla’s DNA. It is not driven by accounting goals, but by strategic goals and efficiency targets, by innovation. The best and the only way to cut cost without loss of competitiveness is through inventing new manufacturing methods, new materials, new processes, smarter robots and workflows. Everything is measured on merit, backed by trial and error, and comprehensive testing.

The battery is the heart of all Tesla automotive products. This is the single most important, non-computing element of any EV that makes or breaks manufacturing cost-based competitiveness. The long term survival of any EV maker depends on it.

On the question of how 4680 battery system is working at Texas 4680 Factory, the answer was surgical:

“It will have 70% less Capex per kWh when fully ramped. Building anode and cathode factories. 66% less factory per gWh. 25% cost reduction on battery production in Q1. The cost savings are substantial”.

If you have the technical means of cost control, a global real-time information system and a clear picture of your cost structure, then you can make much better tactical decisions.

Tesla has unparalleled pricing speed:

Q: “What is the process for auto pricing adjustment?” A:”Tesla has one day latency, better than any other company in the world, except Starlink”

However, this is not the most important part of the story. Even if you have the capability of moving prices around on short notice, that gives you an edge, nothing more. The key is to make decisions that directly support of your strategy. At Tesla, that’s big.

Not one analyst insisted asking questions about Tesla’s AI, or software in general. Perhaps they have their reasons, one of which could be not to give away their valuation metrics. One exception is Adam Jonas from Morgan Stanley who asked Elon if Twitter (or the X app) will accelerate Tesla’s business model (to which Elon mumbled a non-answer).

Perhaps they have been conditioned, maybe for good reason, to playing the “I am a sceptic” game for so long about Tesla’s future plans: robotaxis haven’t become reality despite repeated promises (arguably, still far away from achieving that goal), Dojo still hasn’t proven to be as powerful as expected to be, and the humanoid robot project went silent.

The fact is though that Tesla has actually made enormous progress in building the most comprehensive software system, by far better than anyone in the industry. And that is what the earnings call analysts missed, and many investors who criticised Tesla’s decisions to lower their car prices.

Tesla OS Is a Platform.

There is one line in Tesla’s earnings call presentation that was left unquestioned. I haven’t seen it discussed anywhere. Most articles repeat the same story of margins, prices and volume, and how Tesla has larger room for price adjustment vs its competitors. Cars are cars, right?

Take a look again at Tesla’s operating system. There is one line there that received no attention at all, although it has a major strategic significance. It points to where Tesla wants to go: build an enterprise software platform.

ARK recently published a research paper that estimates Tesla’s share price will be in the $1,400-$2,500 range by 2027. The valuation relies on up to 67% contribution of the robotaxi business in a variety of scenarios from 2023 to 2027. Another contribution built into the valuation is energy storage. The report doesn’t include the potential impact of humanoid robots either as it seems to be a too distant possibility and it is not specifically mentioned in the earnings report.

Tesla Enters the Enterprise Space

Cybertruck production will start before the end of this year in the Texas factory. As Elon Musk calls it, “the hall famer”, it will open a new business segment for Tesla servicing mainly small business operators. Meanwhile the Tesla Semi is in pilot production in the Nevada factory, perhaps planned to enter production next year.

Tesla’s approach to the market is to differentiate their trucks from their competitors’ in the same way they do it in the personal transportation sector: intelligent software.

In the enterprise sector, the differentiation will not be limited to the self-driving capabilities, but as the Tesla Operating System architecture shows, Tesla’s truck will differentiate with enterprise software tools.

We have to remember that Tesla’s vehicles collect vast amounts of information. This is a lean operation, 99% muscle, 1% fat. Nothing is produced by chance. Expect the same pursuit of efficiency to drive the enterprise software development to create useful products for Tesla’s truck owners.

These are software tools that help trip planning, carried items, finance, on duty staff management, delivery scheduling, people management, customer relationship management, profitability. Add to that third party software programs that will compete on TeslaOS for business for other services. This will the Tesla’s AppStore.

That approach to business will be reflected in the hardware architecture. The Cybertruck will be designed to spark the creativity of third party accessory designers who have an in-depth knowledge and practical experience in the field:

Robotrucks vs Robotaxis vs Robodrivers

Robotaxis is a dream term, a dream of autonomous cars roaming around on command. I think it will be a dream for a while. Even if technologically that software is ready, which I have doubts it will be that ready soon, the reality of life in the city has the capacity to invent all sorts of obstacles. These include administrative complexity, resistance by very vocal few opponents, crime, cleanness and maintenance, public health problems, and privacy. I am inclined to believe robotaxis will be adopted faster if they are specifically designed for this purpose: they have to be spacious, more like a mini-bus, high ceiling, simple seating and luggage storage. Like shuttles.

For business, the proposition is entirely different. Long haul trucks, driving on long stretches of uninterrupted highways, self-driving is possible. We can imagine a train of 4-5 Tesla semis driving in perfect synchronicity, entirely autonomous. You can have a human driver in the first car and complete autonomy in the next four vehicles following you around. It makes economic sense. Robotrucks will become reality much earlier than robotaxis

Robodriver, may be a more pragmatic term that describes a Tesla car driving by itself on command or with its owners, friends or relatives on board. It requires far few regulatory hurdles to pass, and it is more acceptable. The demographics in the developed countries are ready to embrace this innovation: the old and the young (statistics show the urban young generation is less interested in owning a car or take driving lessons).

Robotrucks with enterprise software on board are a dream for delivery service companies, and for Tesla. Add to that Starlink service and you have a powerful business model and a very profitable one too, a model that is realistically improvable for many years.

FSD for Tesla Fleet will be very profitable for a long time. When asked about the value of FSD, Elon Musk replied without hesitation: “enormous”. People think immediately robotaxis, but it is the enterprise business as a whole that will make Tesla very valuable.

So, Why Did Tesla Drop the Prices?

Simple answer: because it can. Tesla is one of the few car companies that can do that without incurring loss. As Elon Musk said in the FY23 Q1 earnings call Q&A:

Tesla is in a strong strategic position. We are the only ones making cars that technically, we could sell for zero profit for now and yield actually tremendous economics in the future through autonomy. No one else can do that.

More importantly though, there are strategic reasons, not just tactical:

Increase the AI Training Base

With each sale Tesla gains a training unit that generates large data sets that inform the AI models details about the real physical environment, the behaviour of drivers and surrounding actors, weather conditions, and traffic.

Increase Customer Base

Adding a diverse customer base is critical for AI training and business modelling. The non-transferability of FSD software licence is an annoying quirk for buyers, but the underlying reason is the propagation of that software with each new buy. Its use is addictive because it educates convenience that is difficult to abandon, so customers will buy it again with each new vehicle they purchase.

Compete Against ICE Vehicles not just EVs

Lowering the price will attract customers who are on the edge oscillating between buying an EV or an ICE. Price is a big barrier. By lowering the price the barrier disappears.

There is also another important reason. The major car makers’ ICE divisions that are profit centres that subsidise the EV divisions. For example Ford recent “stellar” Q1 earnings press release revealed that Ford Blue, the traditional business, earned $2.6b, the Ford Pro Fleet $1.4b. At the same time, the EV operations registered a los of $722m. Tesla’s aggressive pricing strategy will hit Ford’s profit centres, making it more difficult to develop the next generation EVs.

The American and European traditional car makers have a strong union base, which will fight any cost cutting measures that affect the workers pay. This is an additional weight that brings down their competitiveness against an unencumbered Tesla entering their ICE patch.

Make Room for the Next Generation

The looming launch of the next generation of Tesla cars will create a larger secondary trading market for EVs, causing more trouble for competitors that have a much smaller installed based. It is likely that the first gigafactory to produce the next generation will be the recently announced new future plant in Mexico.

Prepare the Entrance into the Enterprise Market

The car business is similar to the PC business: enterprise would rather buy PCs with operating systems their employees are largely already familiar with. IBM had the first mover advantage, but it couldn’t promote the OS/2 as a better system for business use because Windows had already a huge installed user base and a thriving ecosystem.

Similarly, Tesla OS will be ready for adoption by enterprise customers as many of their drivers are already familiar with it. Besides, Tesla OS is vastly superior to Apple’s CarPlay or Google Play, which are mainly used as music players, GPS maps, and phone based communicators.

The Big Picture

I will end this short analysis with one observation: Tesla is one component of a planetary web of AI driven businesses: Tesla, Starlink, Twitter and SpaceX. It may not sound like much, but it is.

It is strange, but the media and the public at large are not paying too much attention on this development. Look at the two tweets below and compare them. What do you see?

Isn’t it strange that the first tweet received 227k likes and 38.7k retweets, while the second received only 7.3k likes and 1k retweets over similar period of time?

I don’t know why. Maybe people don’t like business news. Maybe the second tweet was de-amplified on purpose. The “unloved” tweet is so important, a rare statement made by Elon acknowledging his own power: Yes I have access to more real-time global economic data than anyone else in the world. Unusual for him, almost gloatingly, he sent that tweet among others to he Federal Reserve and David Westin at Bloomberg TV.

Another way of looking at it is to compare Bloomberg’s human network of thousands of reporters paid to collect data around the world that powered Bloomberg business news for decades to a new type of global synthetic AI network operating 24x7. Elon Musk’s (and others that rush into this space) AI network increases its reach and capability at a pace that cannot be matched by the old model of human reporting networks.

Tesla is not a car company, but an AI network company that along with Google, Microsoft and Facebook, and other emerging new enterprises, is one of the largest data generators and collectors in the world. However, through Elon Musk, combined with Twitter and Starlink, Tesla has the potential of an unparalleled advantage. As it builds its massive AI computing platform and its own AI computer chip specially designed for robotics (cars, humanoid robots), this advantage will increase its value as more gigafactories are rolled out around the world. At the same time, this configuration has a single red hot critical point of risk.