Investor's Patience Being Tested Like It's 1973

Shaking the piggy bank. Invest in innovation vs reduce headcount.

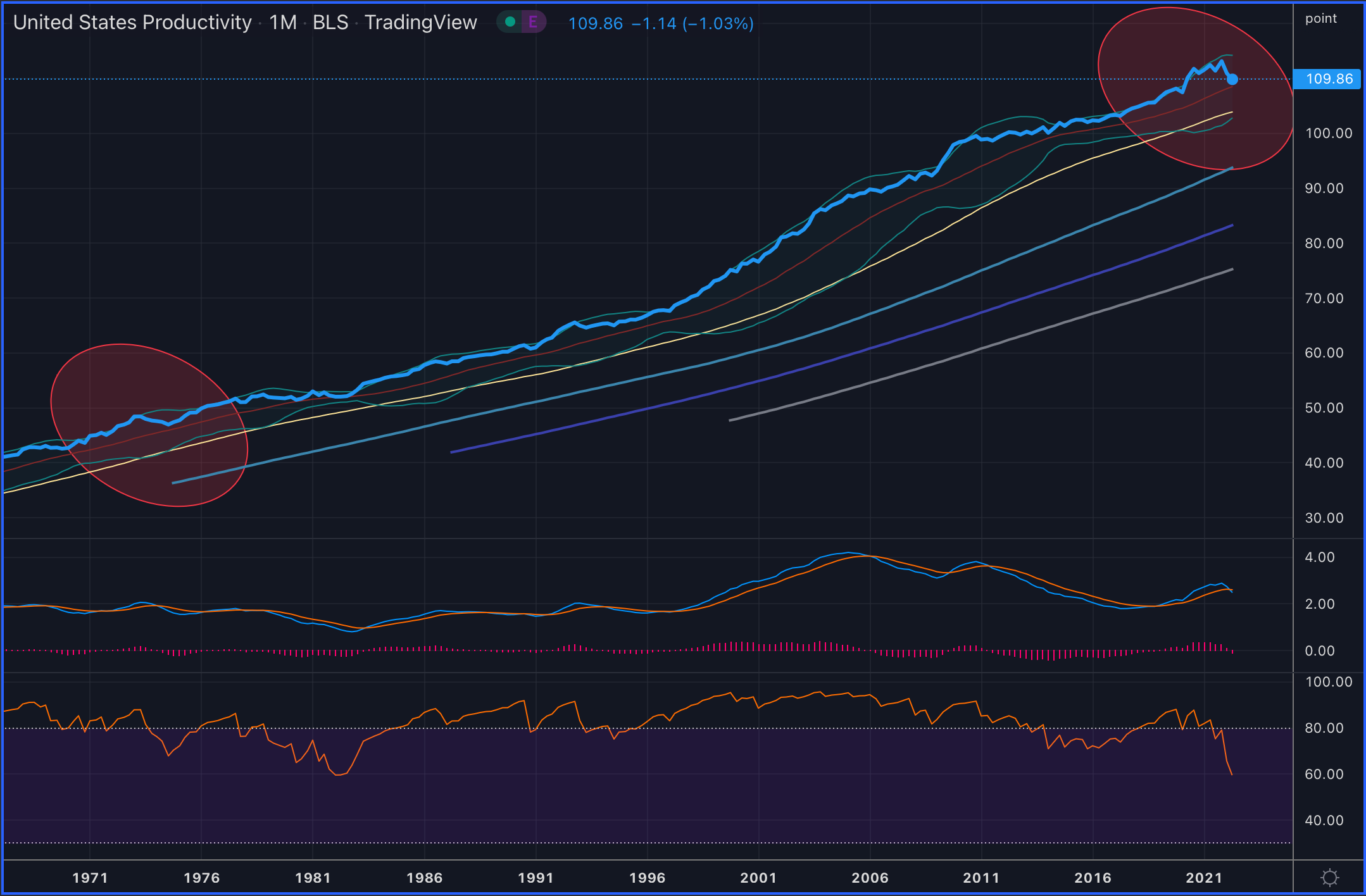

Largest Productivity Drop Since 1973-ish

The last two quarters saw a drop of 3.26% in productivity in US, the largest since about 1973 when it dropped 3.8%, but over a longer time (Mar 1973 to Dec 1974). Similar readings can be seen across other developed economies.

The sharp decline of productivity is supported by a persistent low unemployment which must make the Fed extremely uncomfortable in its pursuit to defeat inflation without causing extensive social damage. Increasing interest rates just doesn’t extinguish inflation unless productivity goes up significantly, and that in turn is hard to achieve without an increase in unemployment, unless a dramatic technological upgrade sweeps the economy.

There are signs that we have to hold our breath for longer while waiting for that technological innovation to have a meaningful impact on the economy. It is clear that a new leadership group is emerging in the stock markets, but it is also clear that we haven’t reached yet the inflection point that marks a definite leadership change.

Two quick case studies: Meta Platforms (META:NASDAQ) and BrainChip (BRN:ASX).

Why Fin Pros Think Meta’s Long Game Falls Short

The contrast between Mark Zuckerberg and professional investors could not be clearer in the past couple of weeks since it has been acknowledged the spending on advertising has dropped due to persistent economic concerns.

There are two interesting aspects here. The position taken publicly by the professional investors to the social media and MSM denotes a bias anchored in an expectation of a guaranteed investment return regardless of the market conditions, a habit formed by Facebook’s historic performance over the years. If you remove the identity of their holding, this is more like a direct request for money (return on investment) that can be achieved by simply cutting costs to increase profit. Whatever happens inside the box representing the object of their investment is not of their concern. The conviction of that demand is so high, they believe that they see something the business is incapable or unwilling to see, something so simple, that can be fixed through cutting costs. They offer abundant advice how Meta should “fix” this problem.

This would make an interesting study in behavioural economics. It also highlights one of the tendencies of many institutional investors to focus solely on finance, macro factors, trading and investment strategies, ignoring the human leadership, the mechanics of innovation, engineering and technological aspects that make up the business and the economic ecosystem at large.

When Mark Zuckerberg explained in the Q3 earnings call the historic importance of the strategic focus on the platform of the future, his words fell on deaf years. All they could think of was costs and margins over the next quarter and over the next twelve months. They are really asking for Meta Platforms to follow in the footsteps of IBM: generate cash into oblivion.

Commentators on CNBC called his spending crazy, Josh Brown, a CNBC contributor, even referring to him in derogatory terms, a wonder boy obsessed with silly games who needs to be put in his place.

The fact, ignored by many, is that Mark Zuckerberg has made a strategic decision to counteract Apple’s policy on user privacy which had a major impact on Facebook’s advertising revenue, irrespective of the overall economic conditions. It’s a losing proposition to operate in Apple’s shadow both in bad and good times. More importantly, Mark Zuckerberg is seizing the unique opportunity to create a computing platform that will not only free Meta from Apple’s control, but establish a powerful leadership position and create a new technological paradigm like the iPhone, only more powerful.

Meta’s platform has a chance to create a technological revolution on par with the revolution created by the invention of television in the first half of the twentieth century. Many derived the Oculus Pro as being too expensive (“who buys that"?), missing the opportunity in the business space and how communication, collaboration, creativity and business relationships can change with a high definition, high realistic 3D medium which can bring together people from around the world.

The collaboration with Microsoft aimed at bringing Teams onto this platform is a hint for what it is to come. Broadcasting video business programs, education and training will completely change the way we do things.

A couple of iterations of Oculus Pro could result in a device that can replace a laptop and three or four monitors with far better usability. Then of course there are the games, friends coming together from around the world in chats that are close to real life (which Zoom could never attain). All this is made possible by the new AI backend architecture Mark was talking about, and which meant nothing other than a cost item to the financial analysts attending the earnings call.

Meta Platforms Will Overtake Apple Over the Next Decade

Seeing a glimpse of the new AI technologies, creation of digital twins, new forms of business communication and social forms of interaction, and the rapid advance I believe that Meta will overtake Apple over the next decade. I say that not only because of what Meta is doing, but what Apple is not. Tim Cook’s reductionist comment about frivolity of the VR lifestyle, means that Apple is content with maintaining with control of the iPhone empire and related services. Apple’s crown jewel is its own private garden built around iPhone, and it seems to be committed to stay that way for the foreseeable future. Even if Apple wants to adopt a radical new strategy, it will be impossible to do so without a leader like Steve Jobs. Tim Cook has been an exceptional business continuity leader, but not a disruptor. If nothing changes, Meta will catch Apple off guard. Working with Microsoft is more than a smart idea by both Mark Zuckerberg and Satya Nadella, it’s an alliance that has the capacity to break the current order.

One thing everyone agrees though, it takes time. From an investment perspective it is a painful reality, but it is also an opportunity to change.

BrainChip Still Working on Mass Adoption

Akida is the first commercial neuromorphic computing chip. Praised by many, it gained world wide prominence when Mercedes mentioned it used Akida in its 1,000 miles range sleek EV, erasing its superior learning performance.

Since then Akida has been evaluated by many interested parties, with small projects mushrooming everywhere.

The Q4 FY2022 report (the last time BrainChip reported a financial year ending in June, as from 1 January 2023 it will mark the first quarter of its new 2023 financial year in line with the standard European reporting style) stated that BrainChip recorded revenues in excess of $5m, although the cash receipts were under $2m. Based on that information you would expect to see an increase of revenue in the September quarter and a significant bump in cash receipts. Yet, the collected revenue amounted to a dismal $100k. The BrainChip shares collapsed on Friday ASX trading day.

The CEO tried to put the state of affairs in a positive light (“We are seeing the greatest amount of sales activity and engagement in the Company’s history“), but the reality is sobering: “the current global technology market has created economic dynamics that have extended evaluations, decreased budgets, and delayed introduction of new technology“. This statement especially caught my eye: “We remain positive on future market penetration and broad adoption of Brainchip’s technology“. Maybe I am wrong, and read to much into it, but it sounds to me like “we are negative” because “these conditions have created a headwind for our prospective and current customers”.

It is also worth noting that the report puts emphasis on strengthening the IP and “accelerating development of next- generation Akida IP and products to extend our technological lead and market opportunity”. This suggests that there is more work to be done to make Akida more compelling, inspired by the feedback received during the recent evaluations.

I am convinced BrainChip is a leader in edge computing and its products will be adopted in large numbers, but when that inflection point will occur is hard to predict. To be more accurate, that moment is not visible, yet. BrainChip needs a couple of high profile successes in the application of Akida, something that results in a significant economic benefit and productivity increase. I am waiting to see that application somewhere soon.

Technological Innovation and Productivity

A successful disruptive innovation happens when the technology has a positive productivity effect. This is the best and the most effective way to reduce inflation. The alternative is an increase in unemployment. Given the geopolitical backdrop is difficult to see which one will prevail in the short term.

The rapid rise of interest rates has a hidden negative effect of inhibiting the spread of innovation by stifling the capital expenditure. Companies don’t invest in times of uncertainty, preferring to adopt an cautious attitude. Look no further than the way investors treated Meta Platforms decision to invest in a future platform.

Central Banks Aggressive Stance Can Slow Innovation

The central bankers need to consider the innovation avoidance effect when deciding how fast they want to raise the interest rates. If they remain hawkish, inflation will be inevitably tamed with high unemployment. If they adopt a moderate stance, they give time to companies to invest in innovative technologies to help them produce more and reduce costs in a constructive way. I hope we see a change toward moderation this month, before the Fed goes into the long break in the new year.